About

We analyse the latest energy scenarios informing UK and EU policy-making, and compare these with the announced US target for a zero-carbon electricity system by 2035. Commonalities offer insights into the actions required in the next 10-15 years to align with mid-century net-zero targets.

Executive summary

A key milestone on the route to Net Zero

The stage is set for a high-ambition coalition on zero-carbon power by 2035 to emerge. Actions taken by this coalition could drive emissions reductions in the next decade, while adding integrity to net-zero targets.

Energy & Climate Data Analyst, Ember

There’s an emerging consensus among climate leaders that zero-carbon power systems in the 2030s are essential for net-zero. The idea that clean electricity can be a foundation for economy-wide decarbonisation is not new, but now it has entered mainstream thinking. Leaders committed to mid-century climate neutrality should heed the emerging consensus and join the US in targeting zero-carbon power by 2035. A high-ambition coalition could play a pivotal role in beginning to align policy and finance towards this goal.

Background to this briefing

Clean power no later than 2035

Soon after taking office, President Biden issued an Executive Order on Tackling the Climate Crisis at Home and Abroad. This included the promise of a “carbon pollution-free electricity sector no later than 2035”. The pledge is reaffirmed in the updated US NDC, released during the Leader’s climate summit.

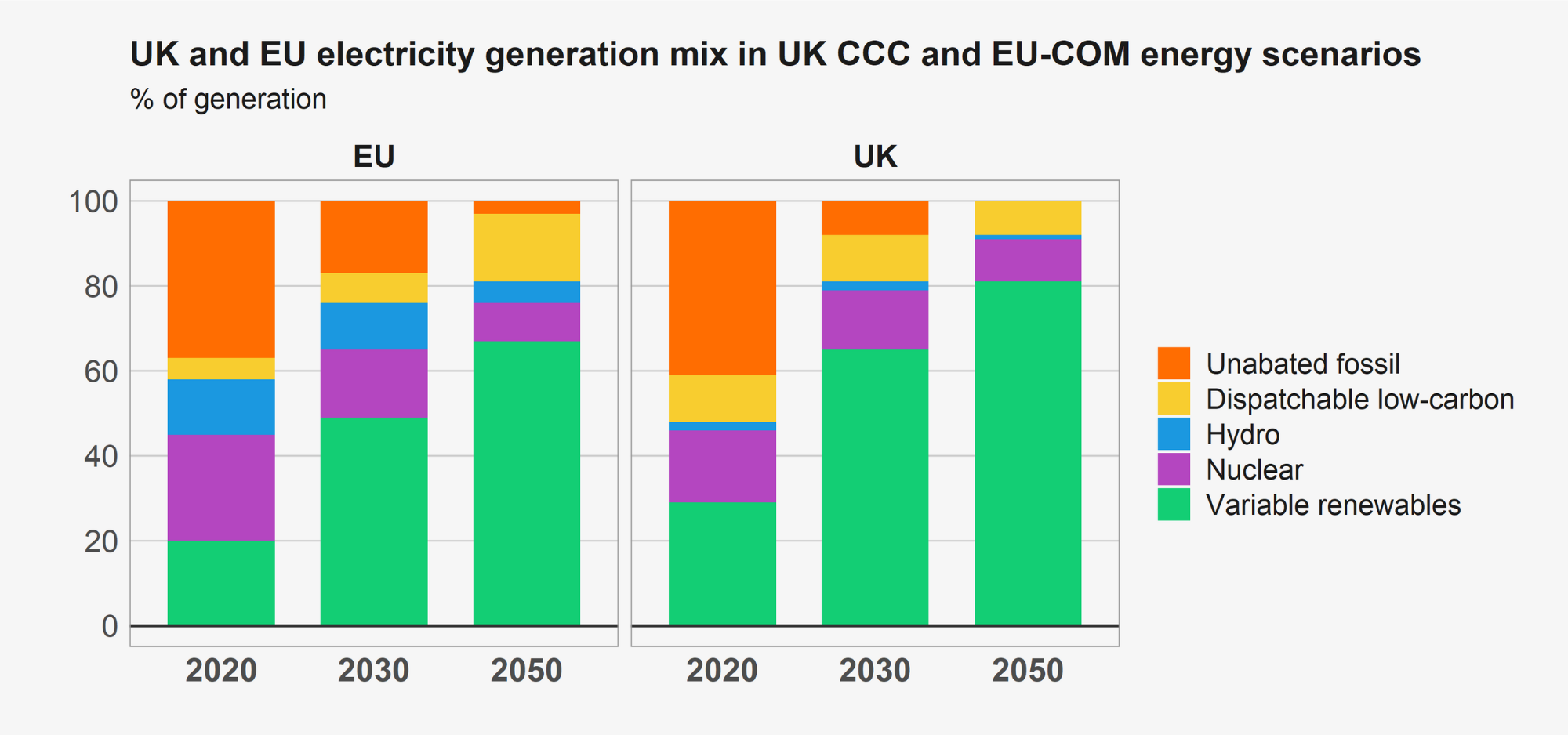

This target is the first of its kind from a major economy, however, in this briefing we reveal the US isn’t alone in aiming for a zero-carbon electricity system in the 2030s. Official analyses by the UK’s Climate Change Committee (CCC) and the EU Commission (EU-COM) both point towards very low carbon electricity by 2035 or soon after. Like Biden’s 2035 power target, the implications of the UK and EU analyses are yet to be fully reflected in policy, but they tell a common story that reaching net-zero emissions by 2050 requires a zero-carbon electricity system long before that date.

Recent years have seen a growing number of countries commit to net-zero by mid-century. On the eve of the Leader’s climate summit, 29 countries (plus the EU) were committed to net-zero, including half of the OECD (21/37 members). While this is encouraging, anticipated emissions reductions in the next decade are not sufficient to remain on track to meet the Paris goals. Key to getting the world on track will be phasing-out coal from global power systems, starting with OECD nations no later than 2030. The emerging consensus revealed by this briefing suggests the time could be right to extend a similar benchmark to all fossil fuels by 2035.

Comparing plans for power

The road to 2035 in the UK, EU and US

In this chapter:

Zero-carbon power by 2035: a new challenge for the OECD

Are OECD countries headed towards the 2035 milestone?

In the wake of the US leaders’ summit in April, and in advance of COP26, the stage is set for a high-ambition coalition on zero-carbon power by 2035 to emerge.

Conclusion

A stepping stone on the way to Net Zero

Taken together, EU, UK and US energy plans reveal a consensus among climate leaders that zero-carbon power in the 2030s is a necessary stepping stone to net-zero by 2050.

While the economic logic for this is well established, and the same conclusion is reached by many other contemporary studies, seeing it borne out in official policy analyses brings into focus the immediate actions required. Given the long timescales involved in deploying electricity infrastructure, and the long lifetimes of assets, it is paramount that policy and finance begin to align with this zero-carbon power future today.

The direction of travel in all three power systems is set towards major reductions in coal generation by 2030, followed by varying but substantial reductions in fossil gas. The UK and US appear aligned on an exit from unabated fossil gas by 2035, while the EU leaves room for a marginal role. Solar and wind grow rapidly to become the dominant sources of electricity in the UK and EU from 2030, and the same is possible in the US. The importance of expanded grids and storage is emphasised across all scenarios to incorporate large shares of wind and solar. All scenarios feature a mix of controllable, low-carbon sources of electricity. The precise mix of CCS, nuclear, bioenergy, or hydrogen appears to depend on uncertain technological progress, future costs, and political priorities.

Despite an increase in mid-century net-zero targets, we find evidence that OECD countries are falling short on key clean power targets in the near term. In the wake of the US leaders summit, and in the run up to COP26, the stage is set for leaders to raise ambition and join the US in targeting zero-carbon power by 2035.

Supporting Material

Downloads

Methodology

Notes on methodology:

- Historic carbon intensities in Figure 1 are calculated using generation data reported in Ember’s Global Electricity Review (2021). Standard carbon intensities for each fuel type were applied for all regions. These were 850gCO2/kWh for hard coal, 1050gCO2/kWh for lignite (EU only), 400gCO2/kWh for fossil gas, and 650gCO2/kWh for other fossil fuels. A more accurate approach would account for regional differences in intensity by fuel type. However, we found that applying these standard intensities to fuel-specific generation data reproduced reported power sector emissions with reasonable accuracy (within 10%).

- Future carbon intensity for the UK was taken as presented by the CCC for the balanced pathway. It was not possible to confirm whether carbon intensities by fuel are consistent between historic calculations and future predictions.

- Future carbon intensity for the EU supply was calculated using data extracted from the EU Commission’s 2030 Impact Assessment (IA). Power sector emissions for policy scenarios are given in Table 39 of the Annex, from which we take 289MtCO2 for the MIX scenario in 2030. Generation data presented in Figure 46 of the Annex shows approximately 200TWh of unabated fossil in 2050, which we assume to be all fossil gas, and by use of emissions factors estimate power sector emissions of 80MtCO2. The trajectory of emissions between these points is implied from Figure 20. Power sector emissions in 2035 in the MIX scenario are estimated to be 200±20MtCO2.

- Figures 3-5 assume even annual growth in wind and solar capacity to achieve the capacity totals available for 2030, 2035, 2040, 2045, or 2050. This is not equivalent to deployment, which will have to be higher to account for retirements.

Summary of scenarios forming the basis of UK-EU-US comparison in this briefing

UK CCC Balanced pathway

The ‘Balanced pathway’ by the UK CCC – independent climate advisors to the UK government. This is one of several scenarios forming the evidence base for the sixth carbon budget advice to the UK Government. In the words of the CCC, the Balanced pathway “makes moderate assumptions on behavioural change and innovation and takes actions in the coming decade to develop multiple options for later”. In April 2021 the UK Government announced it will accept the advice of the CCC and set a new emissions reduction target for 2035.

EU Commission MIX scenario

The ‘MIX’ scenario presented by the European Commission as part of the impact assessment for raising the EU‘s 2030 greenhouse gas reduction target. This scenario, along with three other so-called ‘policy scenarios’, delivers -55% GHG emissions by 2030. The MIX scenario achieves these reductions by extending the scope of the ETS to buildings, road transport and intra-EU aviation and maritime navigation. It also models a ‘medium’ increase in ambition in renewables and energy efficiency policies. In April 2021 the -55% target – informed by this impact assessment – was agreed by co-legislators on the European Climate Law.

US – UC Berkeley ‘90% clean’ scenario (2035 report)

In lieu of any detail about how “carbon pollution-free power” by 2035 will be achieved, we consider a range of analyses. One of the few studies to focus specifically on the 2035 target is the 2035 report by UC Berkeley (UCB), which presents a ‘90% clean’ scenario, whereby 90% of electricity generation is provided by clean sources, i.e., sources not producing carbon emissions (a category in which the authors include bioenergy).