Spot market LNG purchases can cost Bangladesh about $11 billion between 2022 & 2024

Solar could have reduced these imports by 25% and saved about $2.7 billion

Aditya Lolla Senior Electricity Policy Analyst, Ember, Asia

Bangladesh can turn the current power crisis caused by the spiralling gas prices into an opportunity. Redirecting its efforts to ramp up renewable energy capacity and grid augmentation investments now can solve so many problems. It will reduce the country’s reliance on expensive LNG imports, offer protection from global fossil energy price fluctuations, reduce the fiscal burden on the government, improve overall energy security and place Bangladesh in a stronger position in climate negotiations.

Dr Achmed Shahram Edianto Electricity Analyst, Ember, Asia

Renewable energy, especially solar, represents a low-risk diversification option when compared to other fossil energy sources. Once installed, domestic renewables offer Bangladesh control over its energy and protection from global market volatility.

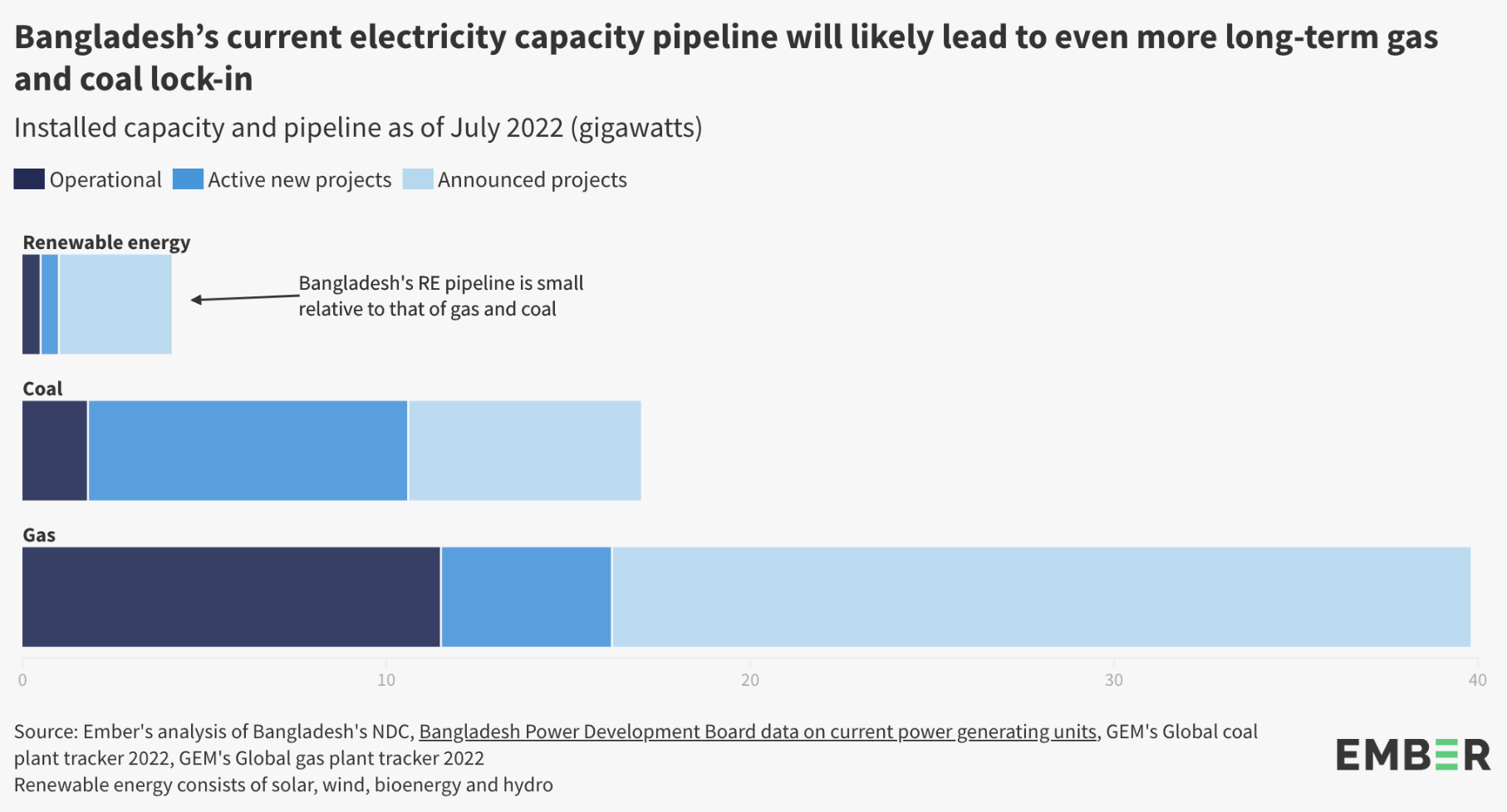

USAID pegs Bangladesh’s total solar potential at 240 GW. But ramping up solar capacity could be challenging and will involve ancillary costs. Lack of land availability to install solar power plants is an issue, but the government has options to address this. Apart from this, it will need key investments in new grid infrastructure, reinforcing distribution grids and building necessary flexibility to increase the hosting capacity for solar. The good news is that solar and battery/storage technology are getting cheaper every year, and their prices are expected to continue to decline further this decade.

A practical breakthrough is also required to allow the RE market to grow. For this, the government needs to address various supply-side issues such as insufficient grid infrastructure, lack of flexible capacity to accommodate rising outputs from variable renewable energy, and oversupply in the domestic electricity market.

For Bangladesh to shake off its fossil fuel reliance and build a sustainable, reliable and affordable electricity supply, especially solar, international financing in RE and flexibility is absolutely critical. Investing in solar makes sense for the financiers too as the investments are likely to be paid off quickly.

India is currently building solar power plants at an average cost of $560 million/GW. Even if such projects cost 50% more in Bangladesh and if we assume flexibility and grid augmentation costs double the overall project cost, about 6.5 GW of solar could still be installed with the same $11 billion, which Bangladesh might have to spend on spot market LNG purchases in just 3 years.

Supporting Material

Acknowledgements

Solar power plant for irrigation at a paddy field in Kustia, Bangladesh

Credit: Muhammad Mostafigur Rahman / Alamy – Editorial

This mini-briefing analyses the current LNG import crisis in Bangladesh brought about by the global gas crunch and the lack of clean energy alternatives. It builds upon the recent news that Bangladesh is finding it difficult to secure long-term LNG supply and is being priced out of the spot market, where LNG is traded for immediate delivery. It estimates the total spot LNG import costs that Bangladesh could incur between 2022 and 2024. Finally it evaluates how much of these imports could have been avoided if Bangladesh built more solar according to the ambitious Mujib Climate Plan.

Featured in the media