About

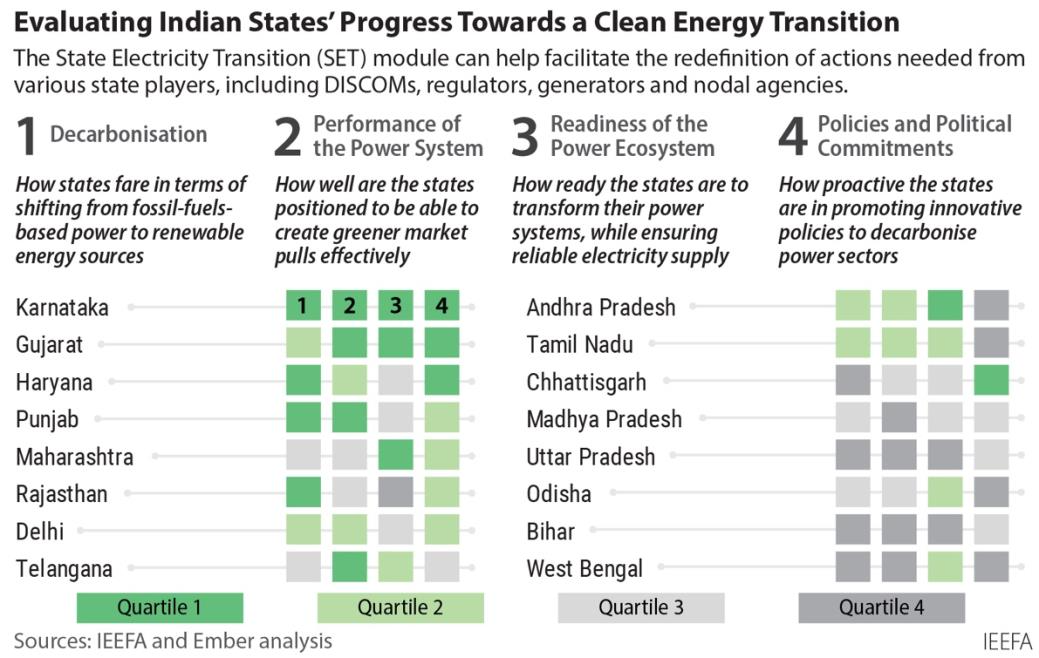

The joint report by the Institute for Energy Economics and Financial Analysis (IEEFA) and Ember analyses 16 Indian states, which together account for 90% of the country’s annual power requirement, across four dimensions. The dimensions track a state’s preparedness to shift away from fossil-fuel-based power, its ability to incentivise greener market participation, its power system’s reliability and its policies pushing for power sector decarbonisation. Based on this analysis, the report authors devised the States’ Electricity Transition (SET) scoring system, which measure the performance of these states relative to each other in the transition to clean electricity.

Executive summary

India is on the right path, but it needs the cooperation of its states

Multi-dimensional efforts are needed to ensure an effective and sustainable electricity transition.

In this chapter:

Saloni Sachdeva Michael Energy Analyst, IEEFA

Bihar, Uttar Pradesh and West Bengal have work to do to strengthen their clean electricity transition performances. These three states should maximise their renewable energy generation potential, and at the same time increase their commitment to moving away from fossil-fuels-based electricity.

This analysis concludes with the following recommendations to accelerate the sub-national electricity transition. A snapshot of the recommendations are:

- Multi-dimensional efforts are needed to ensure an effective and sustainable electricity transition. Efforts are required to decarbonise the supply-side through more renewable deployment and revamp the demand side through energy efficient intervention. In addition, strengthening of transmission infrastructure is crucial for better integration of renewables.

- States should increase participation in green market mechanisms through more favourable policies like open access and banking of power. Innovative bilateral financial markets mechanisms like Virtual Power Purchase Agreements (VPPA) and Contracts for Difference (CfD) have huge potential to open the market.

- State-level data availability and transparency need improvement to measure and track progress. The centre and states need to coordinate better to regularly capture state-level data updates on existing national portals.

- States should ensure effective and timely implementation of clean electricity transition policies like no coal, green manufacturing, direct benefit transfers, green energy open access and more.

Introduction

Transitioning the electricity sector in India

Setting clear pathways for India’s climate actions is critical now.

Vibhuti Garg Director, South Asia, IEEFA

India’s revised Nationally Determined Contribution (NDC) targets have put the country on the right path for transitioning its electricity sector. To achieve those targets, the centre now needs the cooperation of the states to move faster in their clean electricity transitions. This means states redoubling their efforts to walk the electricity transition pathway, and both central and state governments tracking progress and taking corrective measures as required.

Saloni Sachdeva Michael Energy Analyst, IEEFA

The transition now requires cooperation and leadership of Indian states to collectively fight the challenges that impede implementation of the ambitious climate action at the national level.

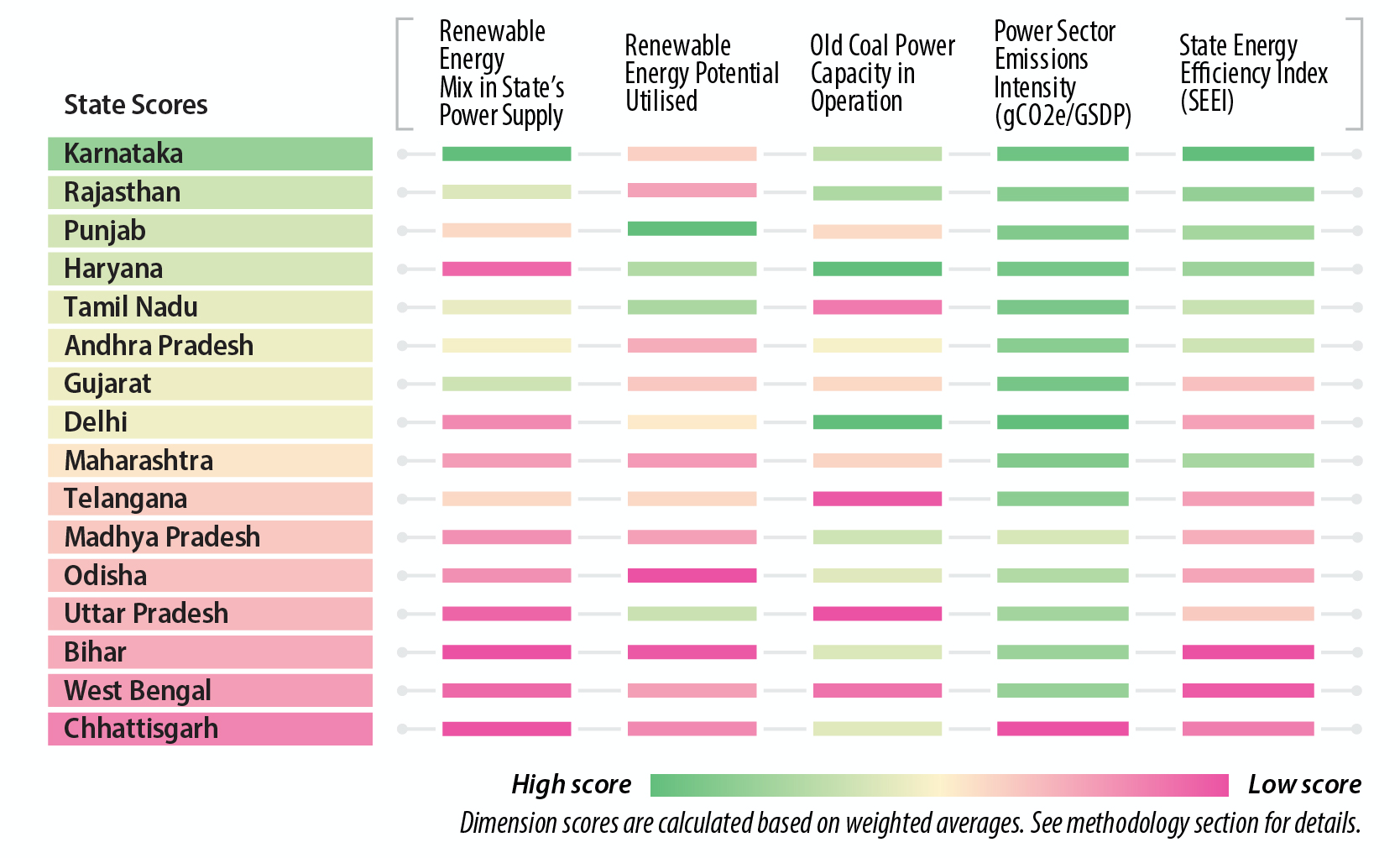

Dimension-1

Decarbonisation

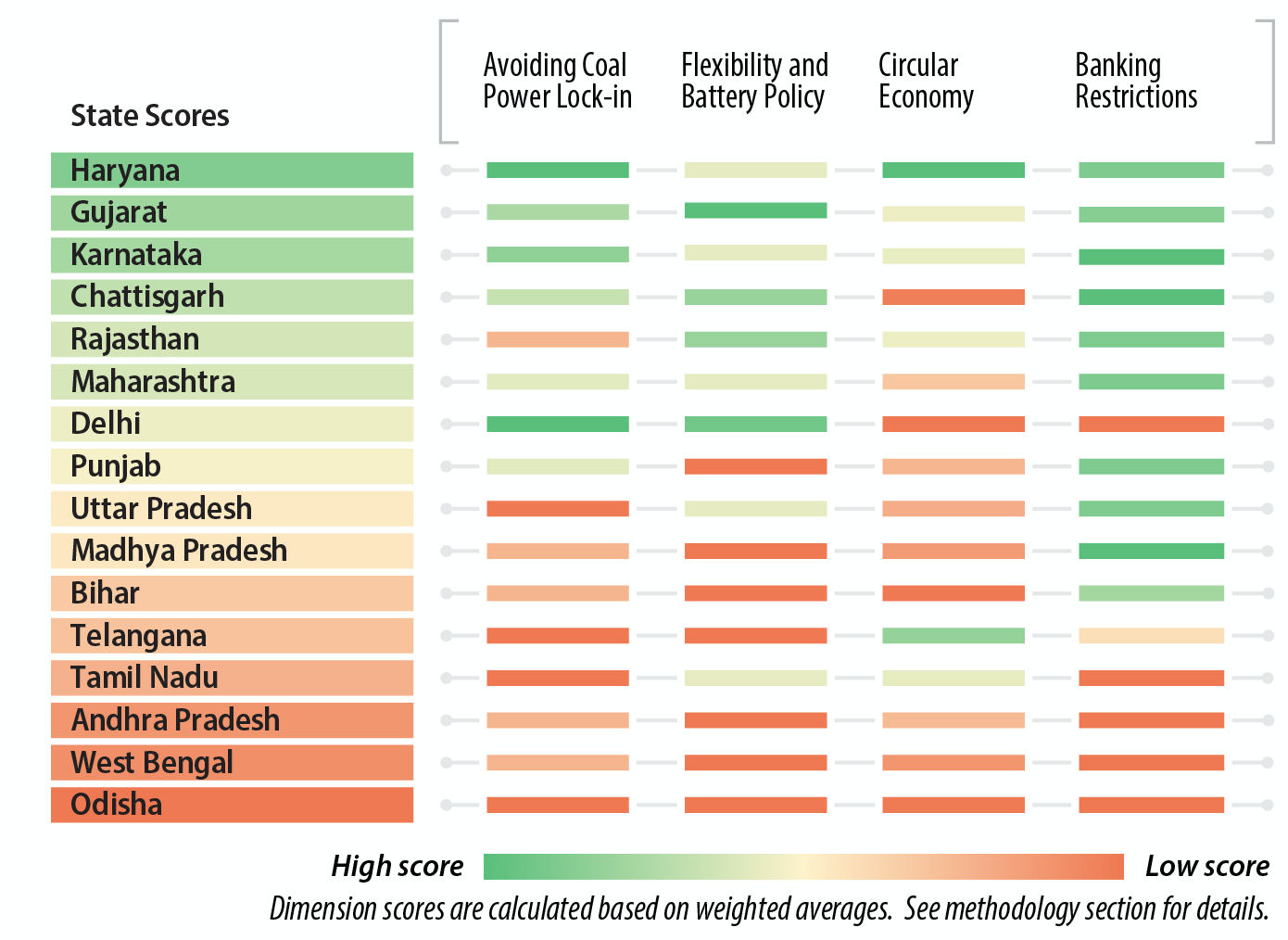

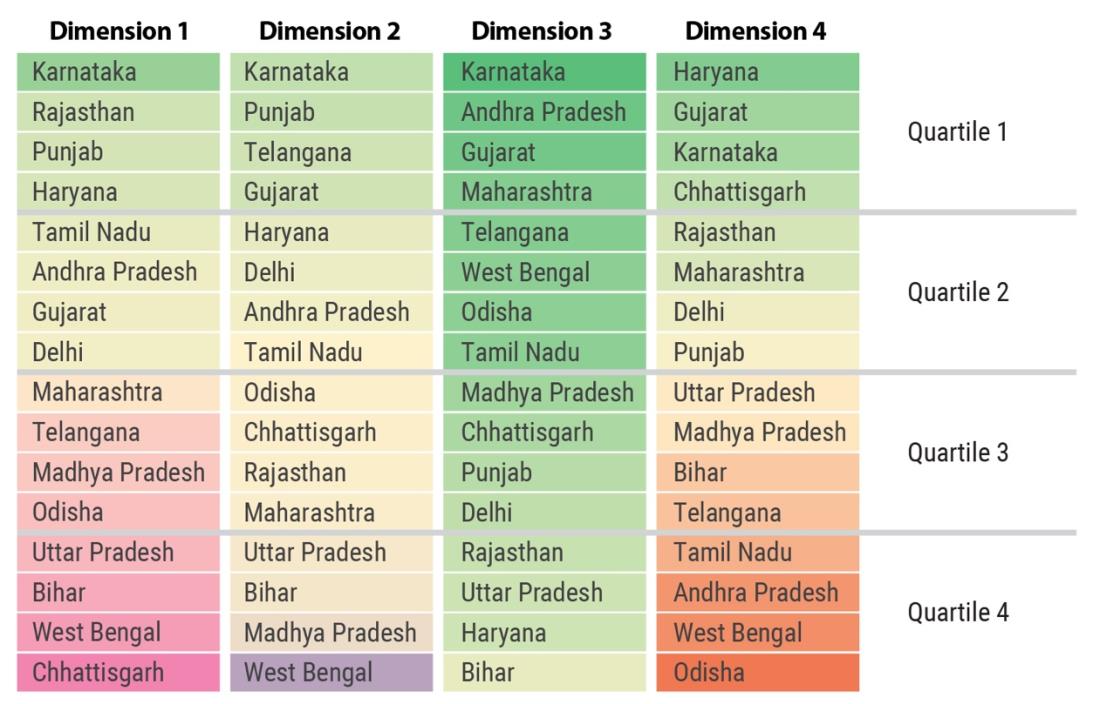

Karnataka, Rajasthan, Punjab, and Haryana performed well across all the parameters.

Gujarat, a state widely regarded as a renewable energy success story in India in recent years, was mid-table in decarbonising its power sector. This is mainly because the fraction of renewable energy potential tapped in the state is still relatively much lower than many other states (10%). Moreover, Gujarat still has a considerable proportion of older coal power plants in its coal fleet (19%), with about 2.9 GW of >25 years coal power plants operational. Both these aspects brought down its overall score.

Maharashtra, with the highest electricity demand in India, was mid-table. This was mainly due to slow renewable energy uptake in the state and the inability to shut down older polluting coal power plants. Its renewable energy share (11%) is lower than most other states. Furthermore, it has utilised just 7% of its renewable energy potential, and about 19% of its operational coal fleet (~4.7 GW) is older than 25 years.

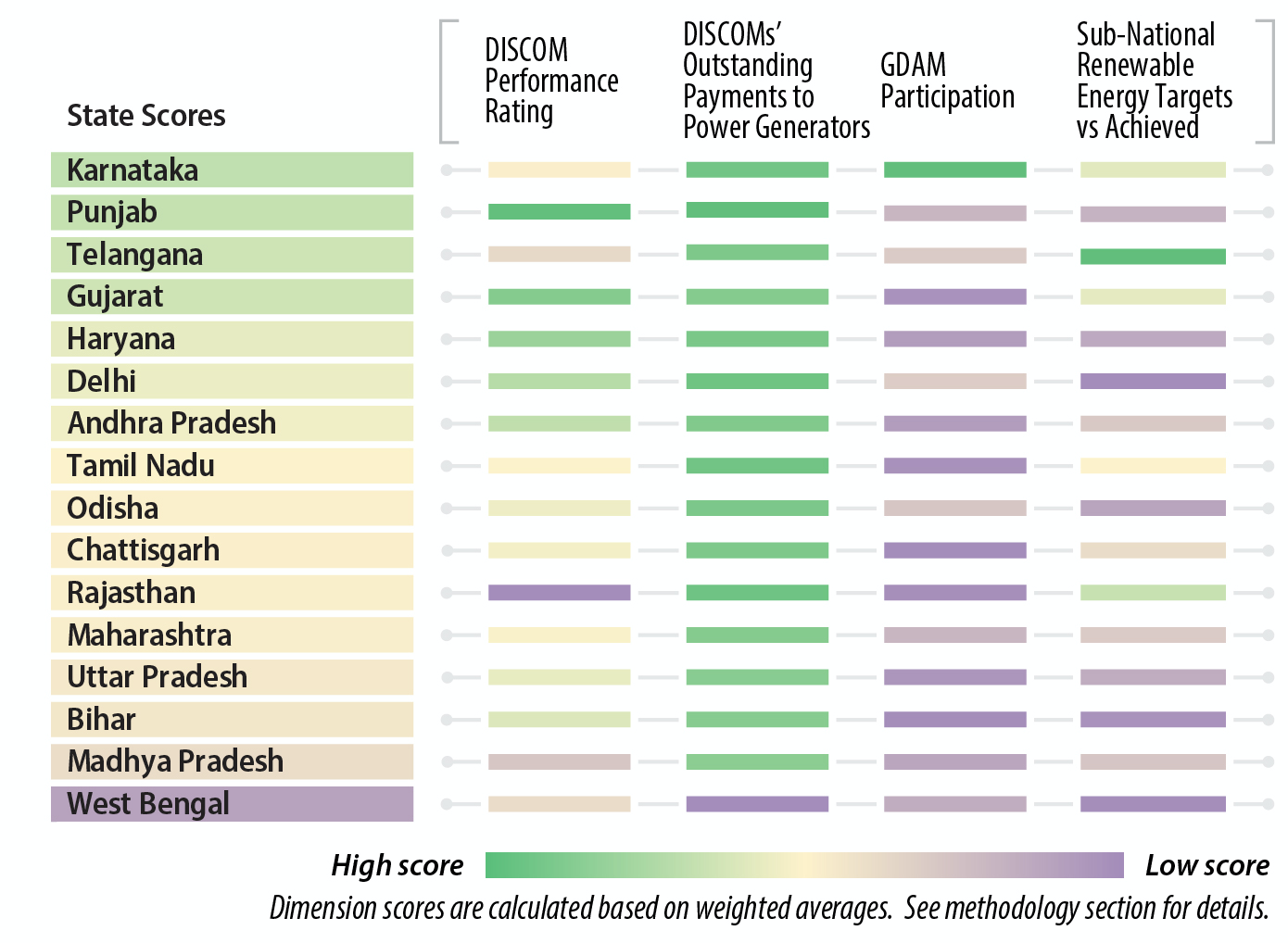

Dimension-2

Performance of the Power System

Karnataka tops the list in this dimension as well. Punjab, Telangana, and Gujarat also performed well on most parameters under this dimension.

Rajasthan and Maharashtra had low scores despite being among the front-runners in initiating various reforms in the power sector. These states have made significant progress over the last decade in increasing generation capacity and strengthening network infrastructure leading to improvements in power supply.

Rajasthan has shown remarkable progress in reducing the AT&C losses of its DISCOMs from a peak of 28% in 2016 to 17.3% by 30 September 2022. Yet, it is still above the target of 15% set under the UDAY scheme. The gap between the average cost of supply (ACS) per unit of power and the average revenue realised (ARR) for Rajasthan DISCOMs has been reducing since FY2013-14. However, they are yet to achieve the target of zero ACS–ARR gap, as stipulated under the UDAY scheme.

Maharashtra, too, fell below its UDAY loss reduction target, with AT&C losses of its DISCOMs at 18.9% as of 30 September 2022. The Maharashtra State Electricity Distribution Company Limited (MSEDCL) also shows a declining trend on most ACS- ARR gap components between FY2019 and FY2021. In addition, the sector’s regulatory assets slightly increased to Rs908.32 billion (US$11 billion) in FY2021, with Rajasthan and Maharashtra contributing 51% and 11%, respectively, of that increase.

Rajasthan and Maharashtra showed low participation in green markets, with just 7 MUs, and 112 MUs, respectively, purchased or sold through GDAM. As seen in Dimension 1, the states have a huge potential to become renewable energy export hubs by utilising their untapped clean energy potential.

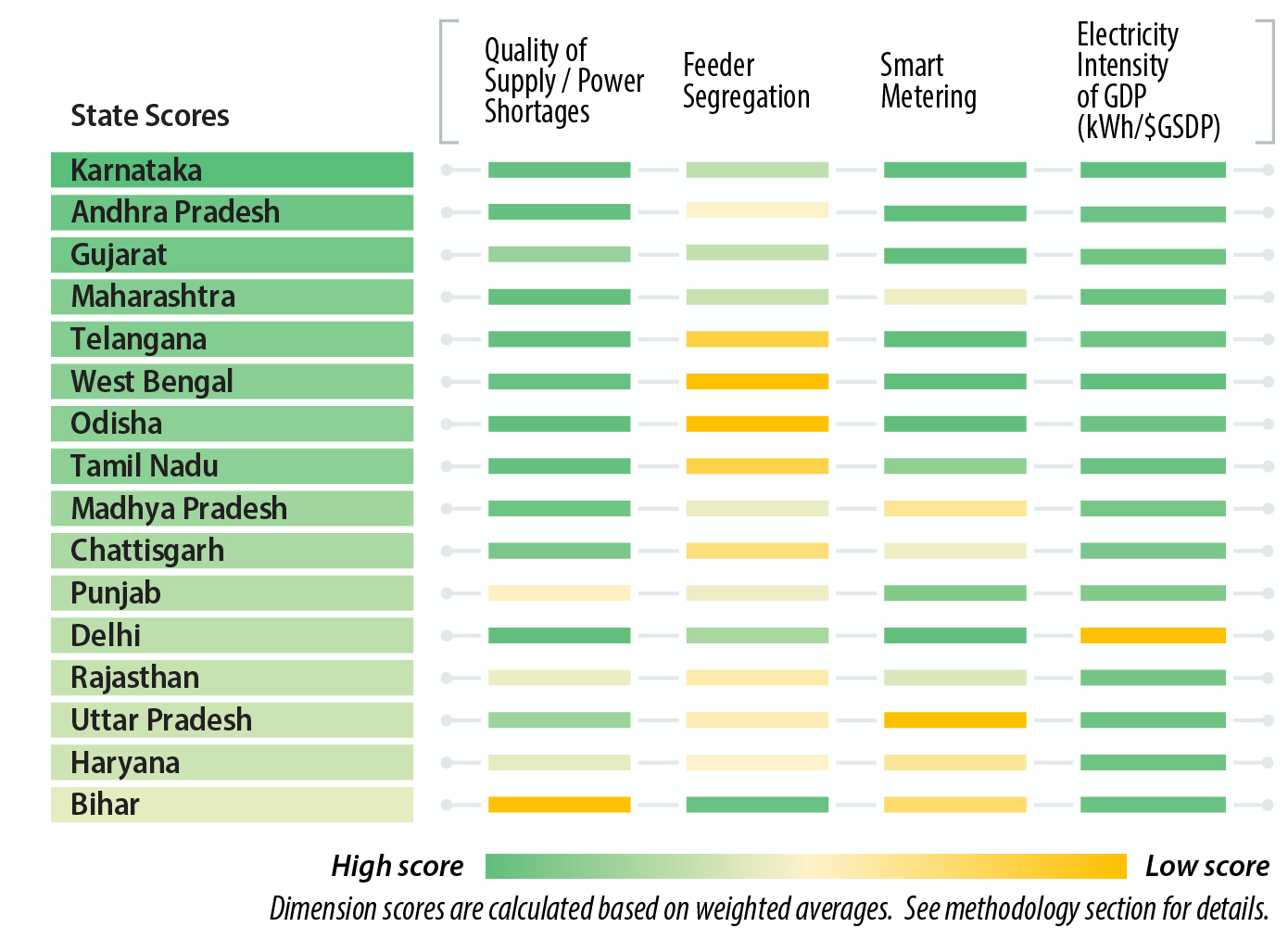

Dimension-3

Readiness of the Power Ecosystem

As in the previous two dimensions, Karnataka leads the way here too. Andhra Pradesh and Gujarat were the other two states whose power ecosystems appear ready for the clean energy transition.

Aditya Lolla Senior Electricity Policy Analyst, Asia, Ember

Even the long-considered front-runners of adding renewable energy capacity, Rajasthan and Tamil Nadu, have to improve the readiness of their power ecosystems for a clean electricity transition. State energy departments also need to strengthen electricity infrastructure for better integration of renewables. In addition to managing the demand and supply of electricity, ensuring effective utilisation, monitoring, and tracking of electrons is also very important.

Aditya Lolla Senior Electricity Policy Analyst, Asia, Ember

Introducing private sector participation and competition would bring more capital and management expertise into the electricity sector. This will help enhance operational efficiency and increase accessibility and affordability.

Dimension-4

Policies and Political Commitments

While Haryana, Gujarat and Karnataka showed good intent to accelerate the electricity transition, Odisha, West Bengal, and Andhra Pradesh still have work to do.

Tamil Nadu, one of the Indian states with the most renewable energy capacity, was in the bottom half of the table in this dimension. This is mainly because of a lack of policy intent to move its future power system away from coal and weak banking provisions, which led to the lowest possible scores on these two parameters. According to GEM, as of June 2022, the state has about 5.7 GW of new coal capacity under construction and 4 GW in the pre-construction stages. The state has been reluctant to commit to no new coal announcements despite studies suggesting that this can save billions of rupees.

Rajasthan was mid-table on this dimension, scoring much lower than other renewable energy leaders like Gujarat and Karnataka. This is mainly due to the state’s inability to commit to not building any new coal power plants despite being in a position to do so. Moreover, the state also has about 2.1 GW of new coal power plant proposals in the pre-construction stages, all of which are state-sector undertakings through Rajasthan Rajya Vidyut Utpadan Nigam Limited. This reduced the state’s overall score significantly in this dimension.

Conclusion

Way Forward

Tremendous efforts have been undertaken by some of the states to walk the electricity transition pathway.

In this chapter:

State-level progress on parameters like open access, green energy corridors, and transmission infrastructure could not be included as part of this study due to a lack of data availability.

Supporting Material

Methodology

The backbone of the SET scores

The backbone of the SET scores is the data dimensions selected, along with the sub-parameters. As stated above, there are four broad dimensions. These dimensions have seventeen parameters in total. A rationale for selection and a mode of measurement backs each of these parameters.

Download the full methodology here.

Acknowledgements

- Saloni Sachdeva Michael, IEEFA

- Aditya Lolla, Ember

- Vibhuti Garg, IEEFA

The authors would like to acknowledge and thank Mr. Abhishek Ranjan (ReNew Power), Ms. Aarti Khosla (Climate Trends), Mr. SC Saxena (personal capacity), Mr. Tim Buckley (Climate Energy Finance), for the constructive feedback provided during the peer-review process.

We are immensely grateful to Mr. Abhishek Ranjan and Mr. SC Saxena for their detailed comments on the data analysis undertaken as part of this study, although any errors are our own and should not tarnish the reputations of these esteemed persons.

We would also like to thank Mr. Akhilesh Magal (Climate Dot), Ms. Disha Agarwal (CEEW), Mr. Neeraj Kuldeep (CEEW), Mr. Ashish Fernandes (Climate Risk Horizons), Dr. Praveer Sinha (Tata Power), Mr. Kashish Shah (Wood Mackenzie), and Mr. Raghav Pachouri (Vasudha Foundation), for their contributions in finalising the report methodology and data analysis process.

Header imageSolar panel trees at the National Salt Satyagraha Memorial, Gujarat, India.

Credit: Indigo Photos / Alamy Stock Photo